How Do Mortgage Lenders Verify Bank Statements

Mortgage lenders rely on thorough bank statement verification to assess borrower risks accurately and prevent fraud. Learn how do lenders verify bank statements with both manual and automated methods and how automation simplifies the process, reduce errors, and enhances efficiency.

Mortgage lending has always got some risks attached to it. However, proper risk assessment can give a clear idea of the risk factors associated with each borrower. It helps lenders to make decisions that make lending almost risk-free. One major step in the risk assessment process is verifying borrowers' bank statements.

Conducting a thorough bank statement verification manually can take up a lot of time. What can we do to make the process quick and accurate?

Let’s understand the ins and outs of bank statement verification and the efficient ways mortgage lenders verify bank statements.

What is Bank Statement Verification?

Bank statement verification is the process of determining how accurate and authentic a bank statement is. It gives an overview of the financial health of the individuals. It plays a crucial part in reducing the risk associated with lending and helps financial institutions to discover any fraud.

The verification involves an in-depth examination of various financial records, transactions, account balances, and other relevant financial activities. It confirms whether the statement submitted is genuine and goes hand-in-hand with the borrower's other financial records.

The information in bank statements can be used as proof of employment, annual turnover rates, and to identify income sources of individuals. The cash flow analysis of bank statements has two main benefits. It will help mortgage lenders understand borrowers' financial standing and assess their ability to repay the monthly mortgage payments.Why Mortgage Lending Needs Bank Statement Verification?

Mortgage lenders are legally responsible for verifying bank statements to ensure the money is not used for illegal activities like terrorism or money laundering. In addition, it provides clear-cut information on borrowers’ overall account balances, an overview of monthly income and debt payments, and an analysis of other monthly expenses.

Thus, by thoroughly verifying bank statements from 2 or 3 months, lenders will understand a great deal about all these aspects and will be able to make better decisions. However, ensuring that verification is done accurately and without errors is crucial.

New technology is being used to forge fake bank statements and scam lenders. Mortgage companies need to be aware of this and find new ways to outrun the fraudsters and the technologies they use.

What does mortgage lenders look for?

Bank statements are used to verify the borrower's financial information. Some of the pieces of information for a verifying bank statement include:

- Account Number

- Account type

- Account holder names

- Open or closed status and opening date

- Balance information, both current and average balance

How to assess the financial health of a borrower? Let’s see how to do it and what information we get during these assessments.

i) Proof of deposit: Lenders use proof of deposit (POD) to verify that the funds required for a down payment have been accumulated in the bank account. The lenders need to make sure the funds are legitimately acquired.

ii) Closing costs: The lender should ensure adequate funds are available in the borrower's bank account to pay various closing costs, such as appraisal fees, taxes, title searches, title insurance, and deed recording fees.

iii) Debt-to-income ratio (DTI ratio): This is a popular metric for mortgage lenders. It evaluates an individual’s ability to manage monthly debt payments.

Debt-to-Income Ratio = Total Monthly Debt Payments/ Gross Monthly IncomeA low DTI ratio means the borrower is managing the debt payoffs well. A high DTI ratio indicates that the individual has too much debt and might encounter problems while paying debts in the future. The highest DTI ratio up to which a borrower can qualify for a mortgage is 43%

iv) Savings and Reserves: The presence of savings and financial reserves indicates financial health. It shows the individual’s ability to handle unexpected expenses and continue with monthly mortgage payments even during emergencies.

v) Large Deposits and Sudden Withdrawals: This is suspicious activity. It requires the borrower to provide further explanations to clarify the source and purpose of such transactions.

vi) Overdrafts and Bounced Checks happen when there is insufficient balance in the bank account during a withdrawal. These are indications of financial instability, and they need careful evaluation. If there are many such occurrences, lending funds to such individuals is not a great idea.

How to prevent mortgage fraud with proper verification?

About 1 in every 134 mortgage applications contain fraud in the second quarter of 2023, as per CoreLogic's latest Mortgage Fraud Report 2023

Mortgage fraud occurs when an individual gives fraudulent information to a mortgage lender to secure a loan they may not get with their original financial standing. Recent technologies are helping to forge documents that look original.

Let’s look at ways to prevent mortgage fraud with the help of proper bank statement verification.

Look for Irregularities in the bank statementCorroborate the bank statement with other documents providedContact the bank to ensure the bank statement is genuineDetect discrepancies in the bank statement with the help of software

How bank statements are verified?

We already know how vital bank statement verification is for mortgage lending. Mandatory bank statement verification is what follows after every mortgage application. It can be done manually or with the help of automation software.

How manual bank statement verification is done?

In the manual bank statement verification, the information on the bank statement for the last 2 or 3 months is analyzed to get a clearer view of the borrower’s income, expenses, debts, and average account balances. This information is cross-verified with other financial documents submitted by the borrower, such as tax returns, pay slips, and employment verification.

In this process, they assess the individual's overall financial behavior. For extra assurances, mortgage lenders may contact the borrower’s bank to verify the authenticity of the bank statement. However, this procedure is lengthy, and the chances of error are still high.

How automated bank statement verification is done?

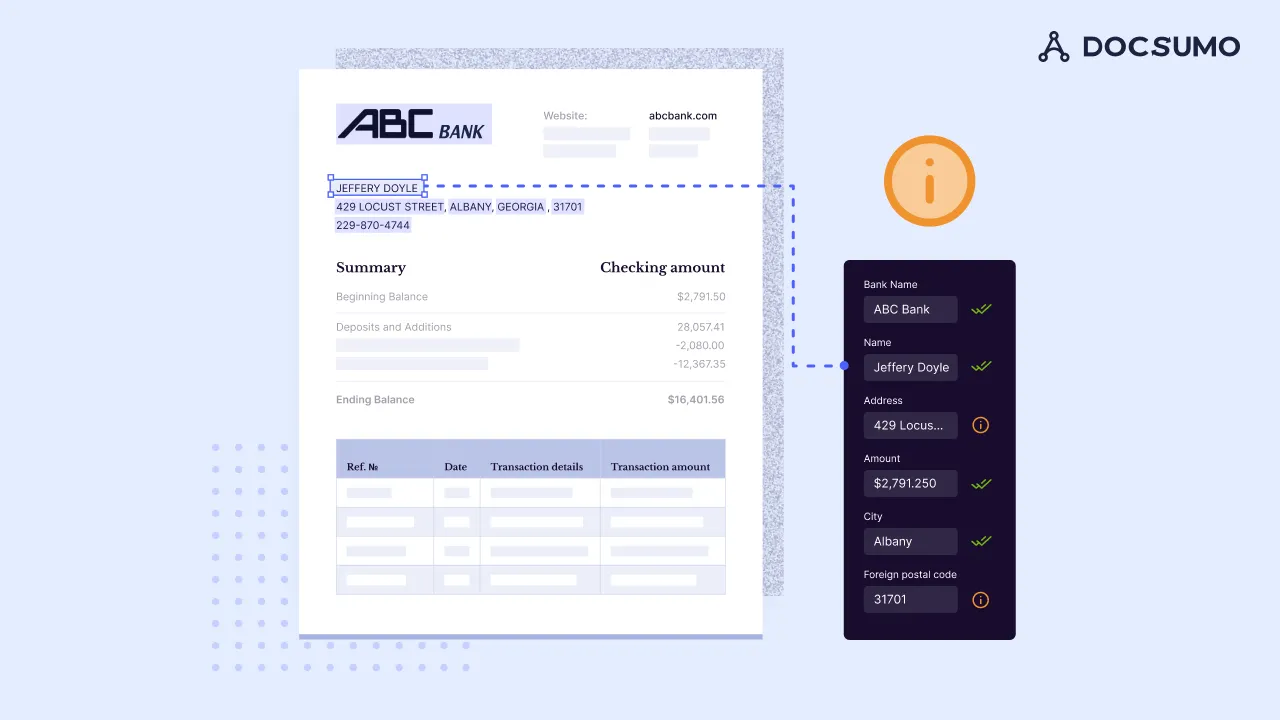

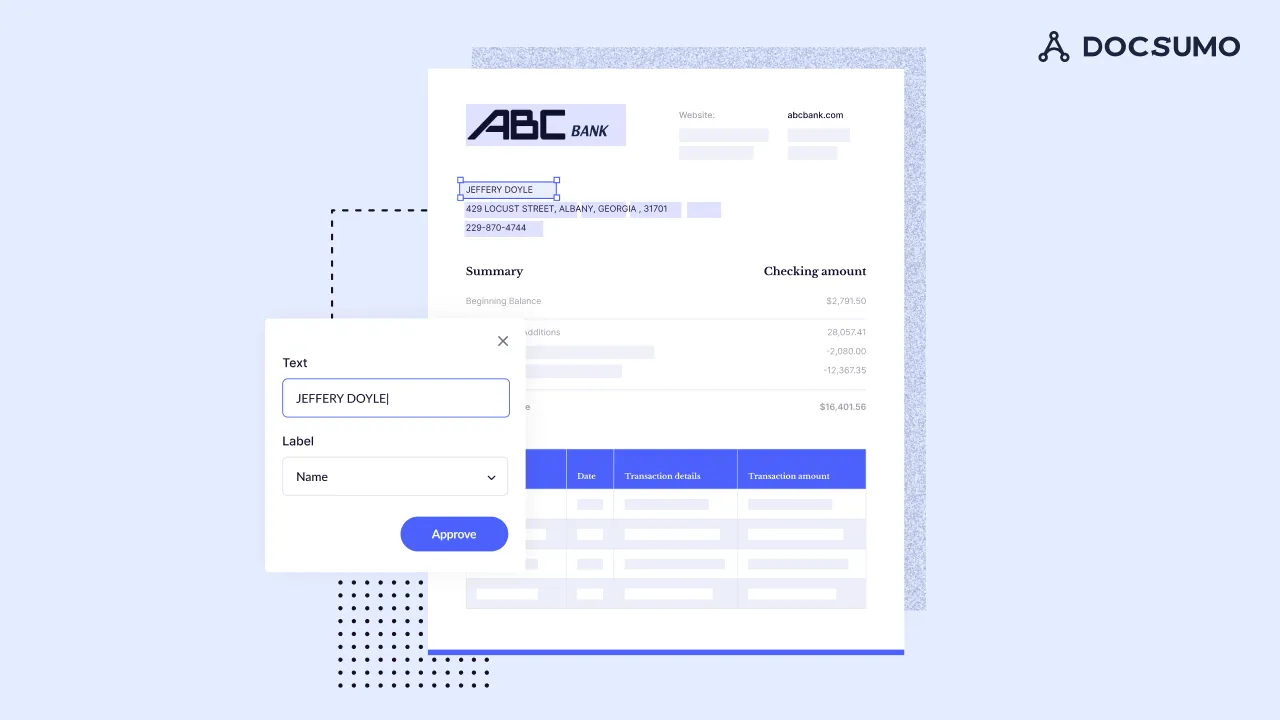

For automated bank statement verification, the data from bank statements is extracted and entered into accounting systems. Then, we perform an analysis on this data using software and new technologies available.

AI software can automatically extract financial information from the statement, validate it, and verify the details entered. Therefore, you save time and effort while keeping the reliability of the process high.

Let’s look at some compelling statistics to see why all financial institutions should embrace automation;

i) 35% of financial institutions report an increase of 2 to 5% in revenues from automating bank statement processing workflows.

ii) Approximately 36% of mortgage companies use robotic process automation (RPA) software to eliminate manual data processing tasks, and more than half plan to expand their use of RPA soon.

iii) 83% of mortgage providers report using at least one back-office automation solution powered by AI.

PayU is a digital lender and leading payment solution provider in India that uses automation to capture data from bank statements. It has helped them save a lot of time while improving their customer experience. These success stories should inspire all mortgage lenders to innovate and introduce automation.

AI-Enabled Automation for Bank Data Extraction

How to automate bank statement verification for lending efficiency?

Automation allows mortgage lenders to focus on high-value tasks by reducing the time required to process the bank statement. They can use advanced algorithms to check the extracted data or identify anything unusual in the bank statement. It makes the operations behind mortgage lending smooth and efficient. Lenders can also integrate bank APIs into their system. Thus, they can directly access and verify the information from the borrower’s bank.

Here are some of the ways lenders can adopt to automate the bank statement verification process:

Template-based Optical Character Recognition Method (OCR): It uses pattern-based recognition for reading and extracting data from bank statements. However, it can only read information from specific document formats.

AI-based or Cognitive Data Extraction: This automation technology learns from previous patterns to make effective decisions. AI can understand a variety of bank statement formats and collect data in a few seconds. It helps mortgage lenders quickly and efficiently deal with the many bank statements they encounter daily.

Combining Machine Learning and Template-based Approach: This model uses standard templates for reading the existing bank statements. When encountering a different bank statement format, the machine learning algorithm learns from it and reads it. Later, it creates a new template for this type of bank statement format without human input. The algorithm gets smarter as it encounters more and more formats of bank statements.

Bank statement extraction software like Docsumo is reforming the mortgage lending industry. Use such software to extract data from unstructured documents with maximum accuracy. Let’s see how a bank statement extraction software works:

Step 1: Extract critical information using intelligent data capture algorithms, AI, and OCR APIs

Step 2: Entering the extracted data into ERP (Enterprise Resource Planning) systems

Step 3: Validating the data. If there are any errors, the API will flag those areas and report them for manual verification.

Why should you adopt automated bank statement verification?

Bank statement verification was done manually in the past. It requires more time and results in borrowers getting impatient and finding alternate lenders. However, with automation solutions, you can transform your lending process. Let’s quickly go through the benefits of automating bank statement verification:

- Reduces the need for paper-based document storage

- Decreases the cost of the whole verification process

- All the data extracted will be safe and secure

- Easy fraud detection with pattern recognitionIncreases accuracy and speeds up the process

- Customer satisfaction as the process is convenient and time-saving

- Bulk document processing

Mortgage lenders can improve and safeguard their functions by automating bank statement verification and other operations while enhancing the customer experience.

Wrapping it up

A thorough bank statement verification is needed to reduce the risk and ensure there is no scam. Using automation is the way to go for any mortgage lenders wanting to improve various processes that are otherwise time-consuming and prone to human error.

Bank statement verification software has already shown how greatly it can impact mortgage lending institutions. Automation will take up all the tedious work and help you focus on what matters.

Now, transform your lending with Docsumo, extract and validate the bank statements with maximum accuracy and efficiency.

FAQs

i) Can a bank statement be verified?

Yes, bank statements can be verified manually or with automation. Manual verification is time-consuming and prone to error, while automated verification is quick, accurate, and efficient.

ii) What are the red flags on bank statements?

Bank statements can give an overall idea about an individual's financial health. After the bank statements analysis, you get a lot of information. A few red flags that mortgage lenders can observe include a high debt-to-income ratio, overdrafts, bounced checks, unexplained deposits, and sudden withdrawals.

iii) Can a fake bank statement be verified?

Technological advancements are in place to forge bank statements and make it look authentic. Manual bank statement verification will not be able to identify fake bank statement. However, AI bank extraction and verification software can find the irregularities in a fake bank statement and report them.

iv) What are the benefits of adopting automation in bank statement verification?

Adopting automation streamlines the process of bank statement verification, making it quick, accurate, and efficient.

v) How many months of bank statements are verified for a mortgage?

Typically, lenders ask for 2 months of bank statements, but in some cases, this can go up to 6 months. For self-employed borrowers, 2 years of bank statements are required.

vi) How do you ensure the funds used to qualify for a mortgage are legit?

The funds should be legitimately acquired and accumulated over time. The fund source should be investigated to ensure the funds for the down payment and closing costs appear over time.