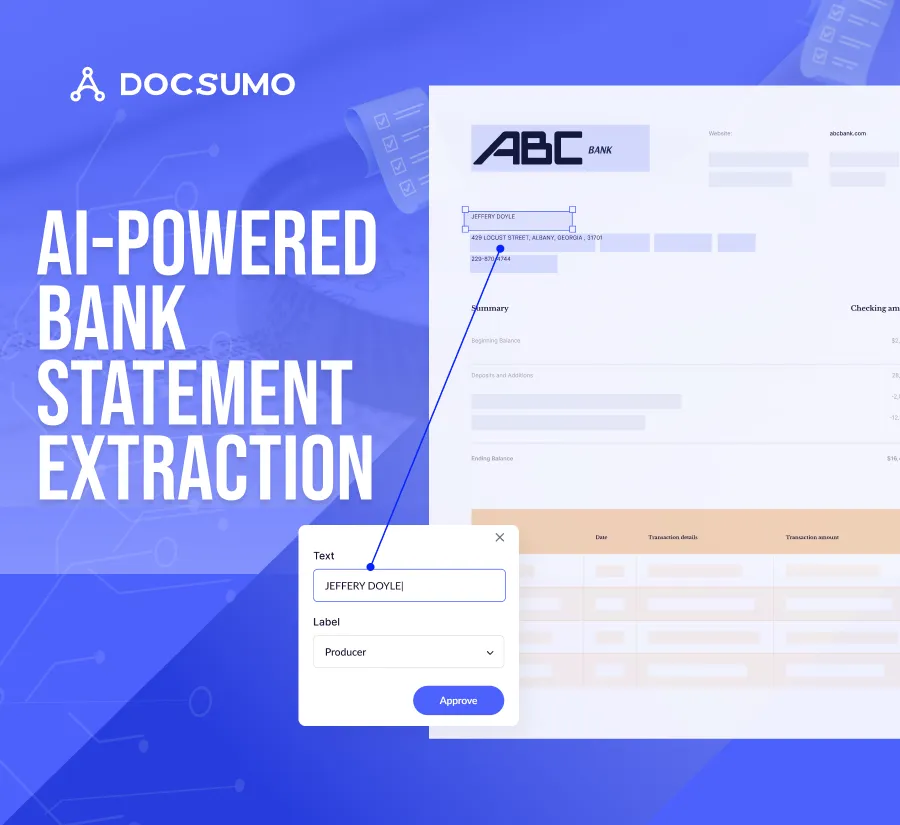

Automate data extraction from your bank statements with 99%+ data accuracy

- Process bank statements in seconds, regardless of format.

- Get your extracted data across two levels of accuracy checks – automated validations and data review for unsure extractions.

- Reduce costs and manual review time by up to 80% with our self-learning AI.

.webp)

.svg)

Test-drive Docsumo’s Document AI

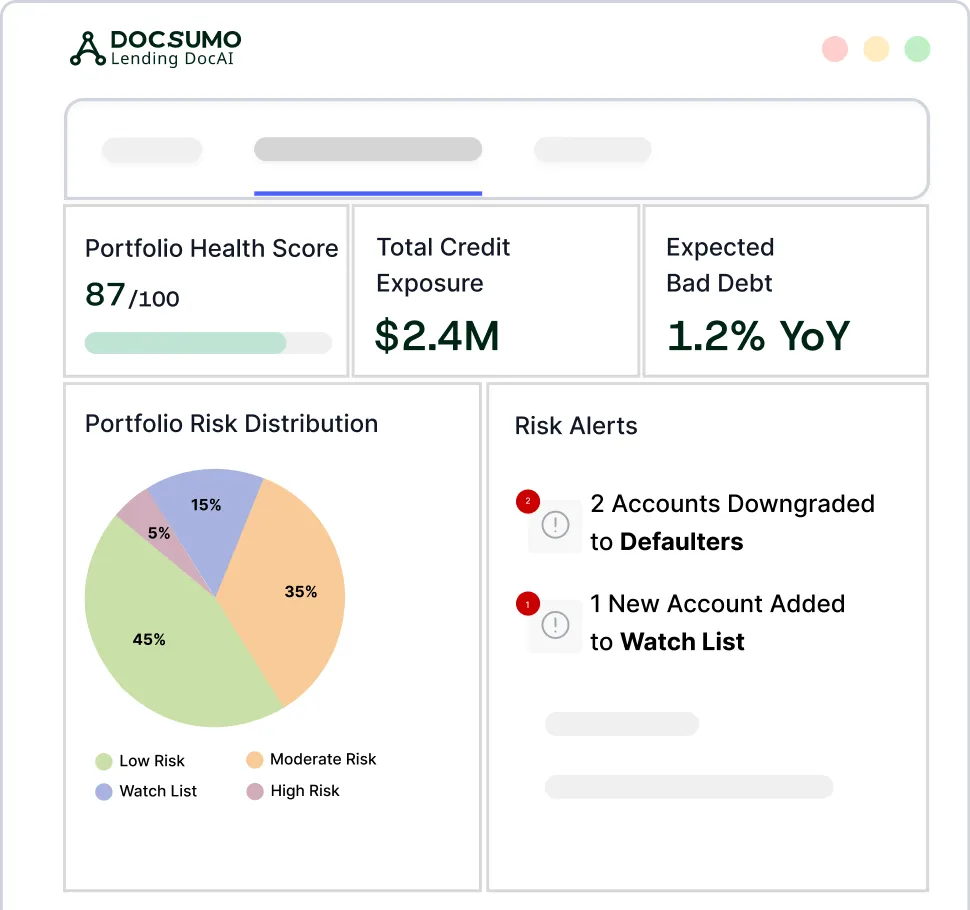

Make faster decisions with insights from your Bank statements

Whether you're looking to process bank statements to reconcile, analyze credit profiles or verify tax reporting faster - Docsumo's intelligent algorithms help you extract the data you need.

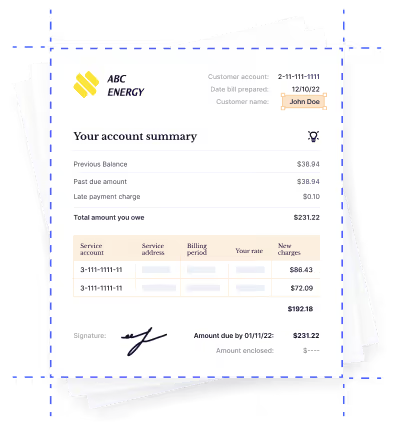

General information

Account Name

Account Number

Bank Name

Opening Balance

Closing Balance

Related information

Start Date

End Date

Account Address

Account Type

Transaction description

Other

Check number

Debit

Credit

Merchant

Other Line items

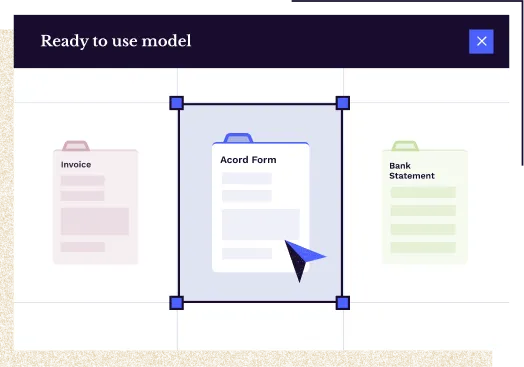

See how it works

Get to know how Docsumo simplifies data extraction for bank statements.

See how we can help your Accounts and Finance teams.

Let's talk.

Docsumo's intelligent document processing enables you to extract data easily, efficiently, and accurately. Fill up the form to speak with an automation expert.